Setting your organizational boundaries is one of the first and most important steps in preparing a greenhouse gas (GHG) inventory. It defines which parts of your organization are included, how much of their emissions you must report, and where to report them.

This decision directly impacts:

- How you account for emissions from subsidiaries, joint ventures, affiliates, and other investments

- Where emissions from leased assets are included: in Scope 1 and 2, or in Scope 3 as upstream or downstream leased assets

Choosing Your Organizational Boundary Approach

The GHG Protocol offers three approaches to define your organizational boundary:

- Equity Share Approach

- Financial Control Approach

- Operational Control Approach

You may choose any of the three approaches, regardless of whether you have operational or financial control over every entity or not. However, once an approach is selected, it must be applied consistently across your entire organization.

At Verde365, we encourage the Operational Control approach, as it is becoming the leading method recommended by CSRD, PCAF, and other major reporting frameworks.

Once you have chosen your organizational boundary approach, continue to the corresponding section below to learn how it works and how to account for emissions under that approach.

Understanding Control Definitions and Lease Types

Before diving into how emissions are allocated under each organizational boundary approach, it's essential to clarify some foundational concepts used throughout GHG reporting: types of control and lease types.

Types of Control

1. Financial Control

A company has financial control over an entity if it can direct financial and operating policies with a view to gaining economic benefits. This often aligns with accounting consolidation and includes situations where the company:

- Has the majority of risks and rewards of ownership

- Has rights to the majority of benefits from an operation's activities

2. Operational Control

A company has operational control if it (or one of its subsidiaries) has full authority to introduce and implement operating policies at a facility or operation. This is typically the case when the company:

- Holds the operating license

- Manages day-to-day operations and can make policy decisions

Lease Types

1. Finance (Capital) Lease

A finance lease gives the lessee the right to operate an asset and assumes nearly all the risks and rewards of ownership. These assets are treated as owned by the lessee and are recorded on the balance sheet.

In most cases, the lessee is considered to have both financial and operational control over the asset.

2. Operating Lease

An operating lease allows the lessee to use an asset (e.g., a vehicle or building) without assuming ownership or associated financial risks.

Typically, the lessee has operational control only, while the lessor retains financial control.

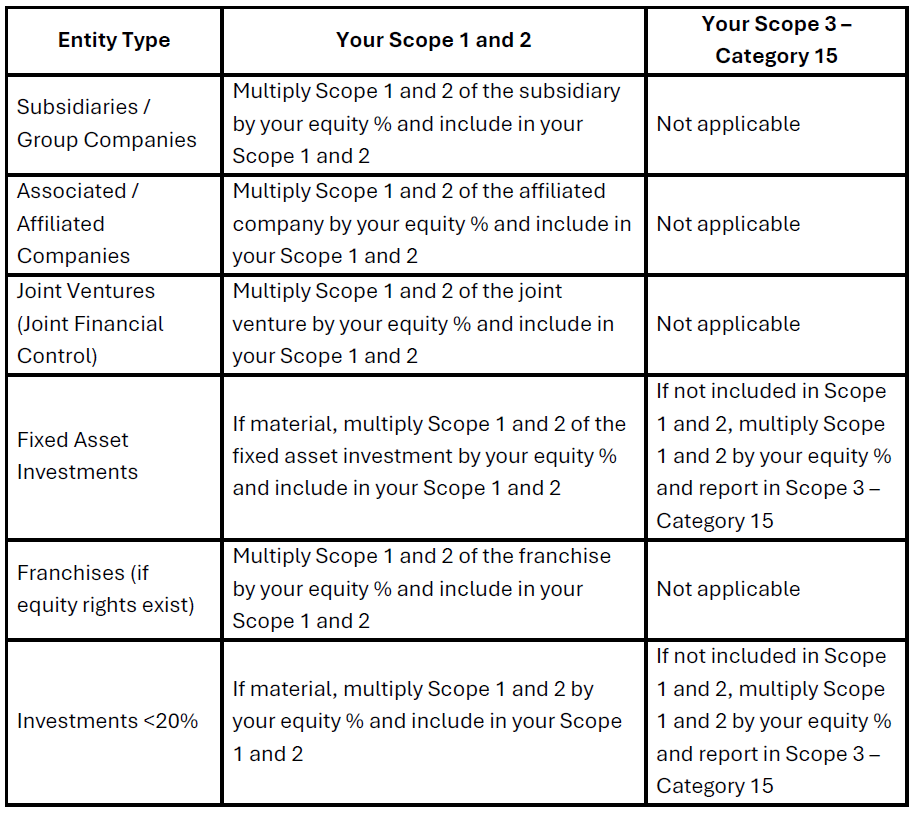

1. Equity Share Approach

Accounting for Group Companies and Investments

You account for Scope 1 and Scope 2 emissions from operations based on your ownership share.

If your company owns 40% of a joint venture, you report 40% of its Scope 1 and Scope 2 emissions in your Scope 1 and 2 inventory. You do not include the investee's Scope 3 emissions.

Accounting for Leased Assets

| Role | Lease Type | Reporting |

|---|---|---|

| Lessee | Finance / Capital | Include in Scope 1 & 2 |

| Lessee | Operating | Scope 3 — Category 8 |

| Lessor | Finance / Capital | Scope 3 — Category 13 |

| Lessor | Operating | Include in Scope 1 & 2 |

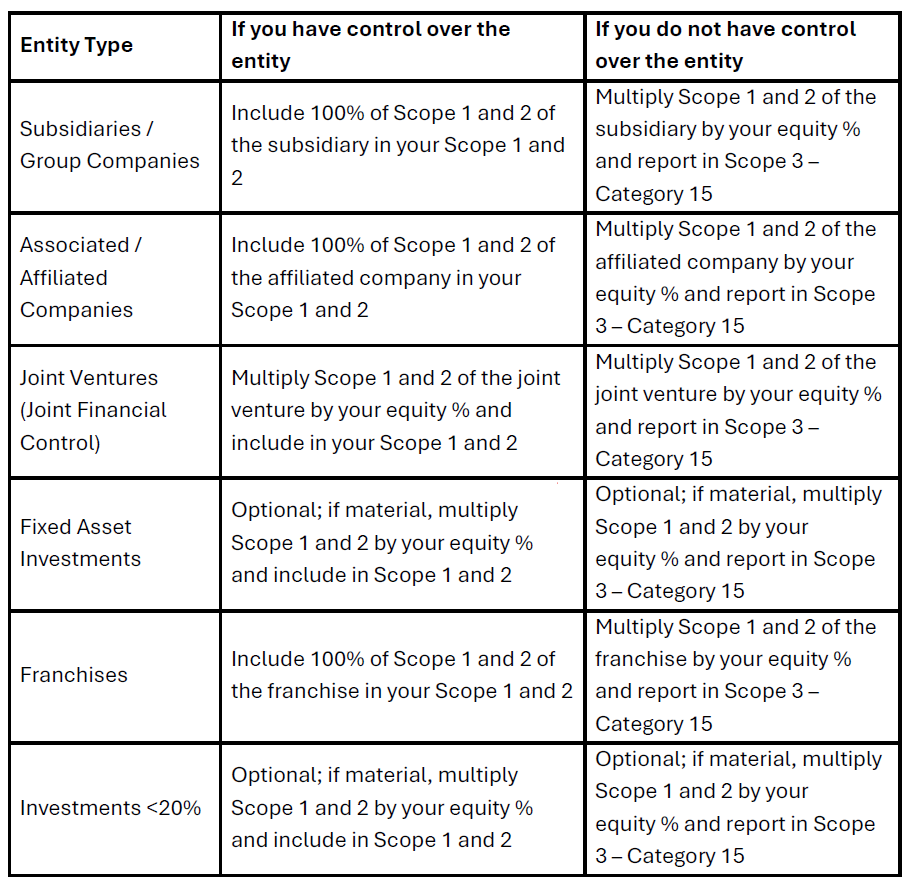

2. Financial Control Approach

Accounting for Group Companies and Investments

You report 100% of Scope 1 and 2 emissions from operations where you have financial control, regardless of ownership percentage.

If you do not have financial control, but own equity, you must report your equity share of Scope 1 and 2 emissions of operations in your Scope 3 — Category 15.

Accounting for Leased Assets

| Role | Lease Type | Reporting |

|---|---|---|

| Lessee | Finance / Capital | Include in Scope 1 & 2 |

| Lessee | Operating | Scope 3 — Category 8 |

| Lessor | Finance / Capital | Scope 3 — Category 13 |

| Lessor | Operating | Include in Scope 1 & 2 |

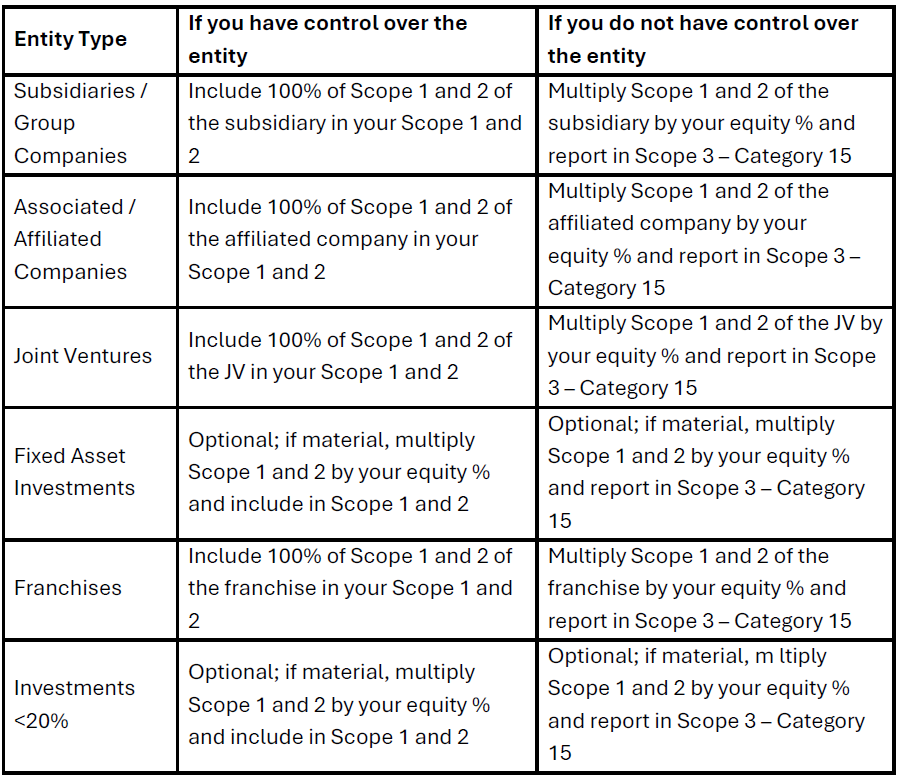

3. Operational Control Approach

Accounting for Group Companies and Investments

You report 100% of Scope 1 and 2 emissions from operations where you have operational control — i.e., where you can set and implement operating policies.

If you do not have operational control but hold equity, you must report your equity share of Scope 1 and 2 emissions in Scope 3 — Category 15.

Accounting for Leased Assets

| Role | Lease Type | Reporting |

|---|---|---|

| Lessee | Finance / Capital | Include in Scope 1 & 2 |

| Lessee | Operating | Include in Scope 1 & 2 |

| Lessor | Finance / Capital | Scope 3 — Category 13 |

| Lessor | Operating | Scope 3 — Category 13 |

How Verde365 Helps

At Verde365, we're building features that help automate:

- The application of equity share, financial control, or operational control across your group structure

- Scope 3.15 emissions calculations from investments

We're committed to making your GHG reporting process simpler, more accurate, and fully aligned with the GHG Protocol.

Need help applying the right boundary approach?

Let Verde365 support your next step toward accurate and reliable emissions reporting.